As we approach the close of 2025, which increasingly looks like a 3rd straight year of double digit returns in the S&P, there continues to be fear and angst about what could go wrong or already is wrong. With that in mind, I wanted to take a look at the year that was and share some thoughts on the road ahead.

After a strong start to the year, Liberation Day came and delivered the worst two-day market performance since Covid and one of the worst in history joining the likes of the Crash of '87 and the Great Depression. Once the tariff uncertainty ran its course, the markets across the board were screaming into the 4th quarter only to be undone once again by the threat/thought of a bubble in the AI space (more on that below). The remaining concern, the Federal Reserve, did their part by cutting interest rates an additional 25bps last week. However, as we go into next year, policy path remains unclear. The odds of a rate cut in January sit at a coin flip right now. In addition to that, the Fed Chair Jerome Powell comes to the end of his term in 2026. Who the new appointee is will go long way in predicting the type and timing of rate cuts we may face, while inflation and labor metrics will also play a large role in those decisions.

One massive uncertainty coming into the year was what would happen with the tax code as the TCJA was set to expire. As I mentioned in last year’s blog, I was operating under the assumption that the TCJA would be extended. Well, it was extended and some nice tax credits were added. Those aged 65 and older are eligible for a $6,000 tax credit (per person) with some income phase outs. Child tax credits have been permanently increased to $2,200. Finally, the SALT cap was temporarily increased to $40,000 which is particularly important in the Northeast with our absurd property tax bills.

There were also changes made to certain retirement and health care accounts that are important to note for 2026. If necessary, be sure to modify your contributions for the upcoming year if your intent is to max out:

- Contribution limits for 401Ks, 403B and 457’s are all up to $24,500 with an over 50 catch up of $8,000, and an additional catch up for those aged 60-63 of $11,250.

- ROTH and Traditional IRA contribution limits were increased to $7,500 with a $1,100 allowable catch up

- HSA contribution limits are up to $4,440 for individual and $8,750 for family coverage (Reminder that you need a high deductible health plan for this.).

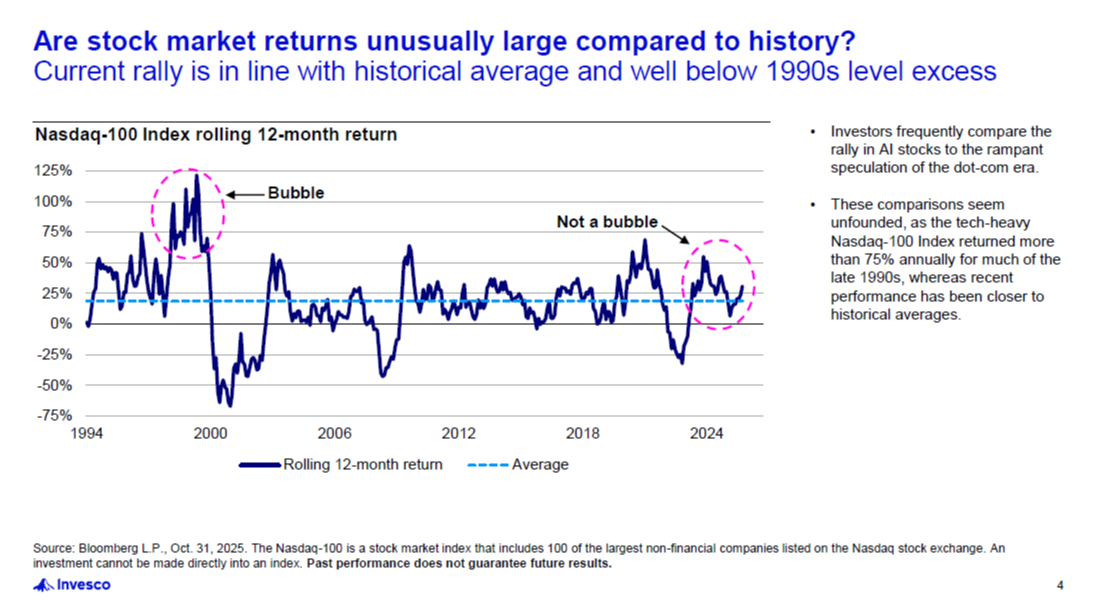

Going into 2026 I see very similar concerns as we exited 2024. There continues to be a delicate dance between labor statistics, inflation and the Fed. While we seem to be heading in the right direction, inflation still seems to pop from time to time which causes negative market reaction and sentiment. However, the overwhelming concern seems to be the fear of an AI bubble similar to the Dot Com bust of the early 2000’s. While it is true that some AI themed stocks are trading at elevated future values, isn’t that the whole point of an investment? You’re betting on future value with what your money is worth today. If you look at the chart below, you will also see that valuations were twice as elevated during the Dot Com bust as they are now.

So, while 33X is a slightly elevated forward P/E ratio it’s nowhere near the levels we saw 25 years ago. I can assure you one thing, the companies that do win the AI race are significantly UNDERvalued right now regardless of what their current P/E ratio is. Look at Amazon’s stock price in 2005. Adding to the glass half full narrative is the strength of the rest of the S&P. Per FactSet, roughly 82% of companies in the S&P 500 exceeded earnings expectations in the 3rd quarter. So, while there are reasons to be cautious, there are also reasons to be optimistic.

As always, and I know you’re sick of hearing it, your plan is YOUR plan. What I wrote above should concern you very differently if you are 25 as opposed to 65. In general, I think there are enough good things in the economy happening right now to feel good about 2026. Having said that, we are about to finish a year that sits at a 16% return in the S&P and it feels like we had a tough year due to the two large selloffs we experienced. The reality is those types of selloffs are normal and representative of a healthy market.

As always please feel free to share this with anyone you think may benefit.