Liberation day has come, followed quickly by Obliteration Day in the markets. Tariff fears sent markets reeling as we come to the closing bell today. It’s certainly a disappointing result after seeing upward trends in the market over the past week.

To recap the first quarter, we saw a cumulative return of -4.6% on the S&P 500 including entering full correction territory off of February highs. Worse, the tech heavy NASDAQ has been in correction territory and closed the quarter down -10.28%. On a positive note, unlike our last sell off in 2022, both bonds and alternatives have provided a hedge against these losses with the broader measure of domestic bonds (AGG) returning 2.06%. This allows for strategic rebalancing for the quarter which I’m working on across portfolios.

I want to address some common concerns I’ve heard moving forward while also pointing out some potential bright spots. Let’s start with stagflation. The dreaded term meaning a slowing economy in conjunction with rising prices and has been an oft recited phrase recently in the media. This is certainly worst-case scenario but also one in which we are going to need to evaluate real economic data in the coming months.

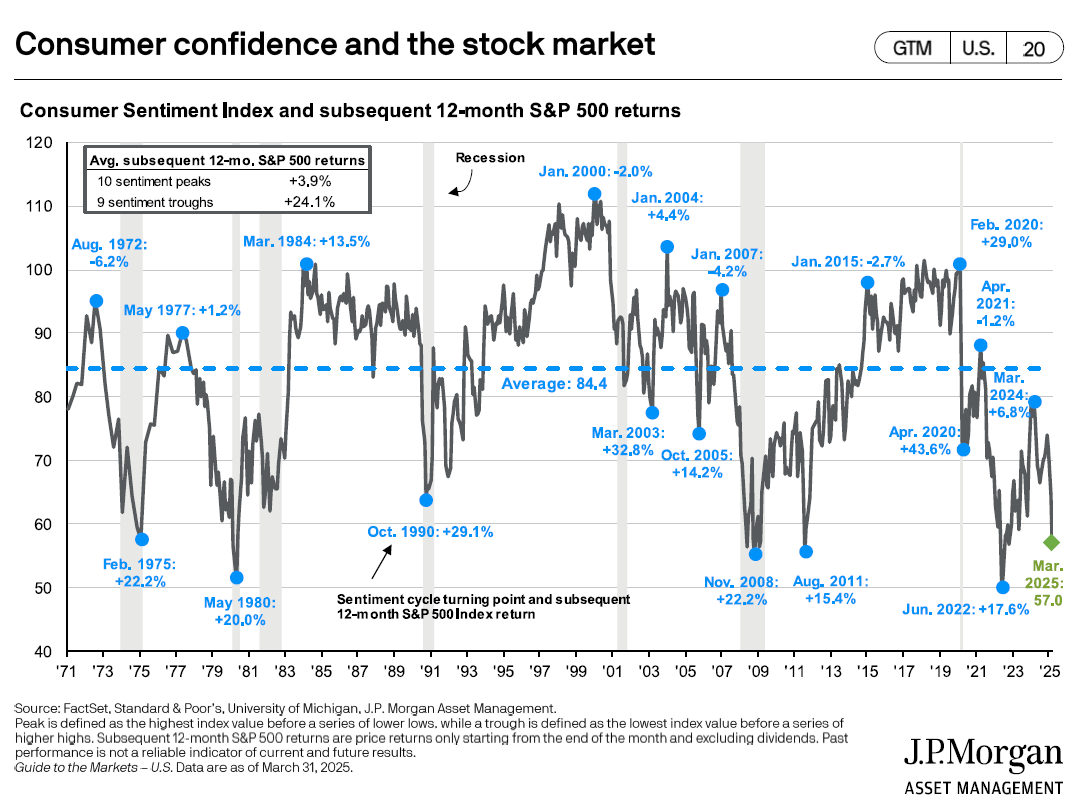

Another big headline was the Consumer Sentiment Index coming in at 57 this week, its lowest level since late 2022. Almost 2/3 of respondents indicated they expect a rise in unemployment over the next year while also showing concerns about inflation being back on the rise. Let’s add a potential bright spot here though. When you look at the below chart, the 12-month S&P return from sentiment troughs has averaged 24.1% compared to 3.9% when sentiment is at its highest. As Warren Buffet famously said, “Be fearful when others are greedy and be greedy when others are fearful.” This will certainly be tested in the coming months.

Finally, we get to tariffs. The big question is this…Is the formal tariff announcement and the corresponding selloff today simply short-term pain that will lead to the next bull run in the American economy OR will it in fact lead to recession, or worse, stagflation. The expectation that Trump 2.0 would focus on the stock market as one of his achievements has been thrown out the window in the short term. But I will add one more bright spot here. One of the administration’s stated goals was to bring down borrowing costs as inflation has remained sticky. We saw the 10-year yield drop below 4% today for the first time since October. That is good news! The bad news? It dropped as investors dumped equities and poured into treasuries.

As I’ve stated on many of these blogs, each of your portfolios is unique, as are your needs. While many hoped for some more clarity yesterday, we have more uncertainty moving forward which is not palatable for the markets and that is showing today. So, as I watch these new policies unfold in real time, we will make decisions together as it relates to your particular plan. In the meantime, if you would like to have a discussion about your individual portfolio don’t hesitate to call me.